Should You Wait for Lower Rates?

Mortgage Rates Laura Miller Edwards Realty Group March 18, 2026

Mortgage Rates Laura Miller Edwards Realty Group March 18, 2026

Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range. If you saw that and thought, “Great. I missed it,” you’re not the only one.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

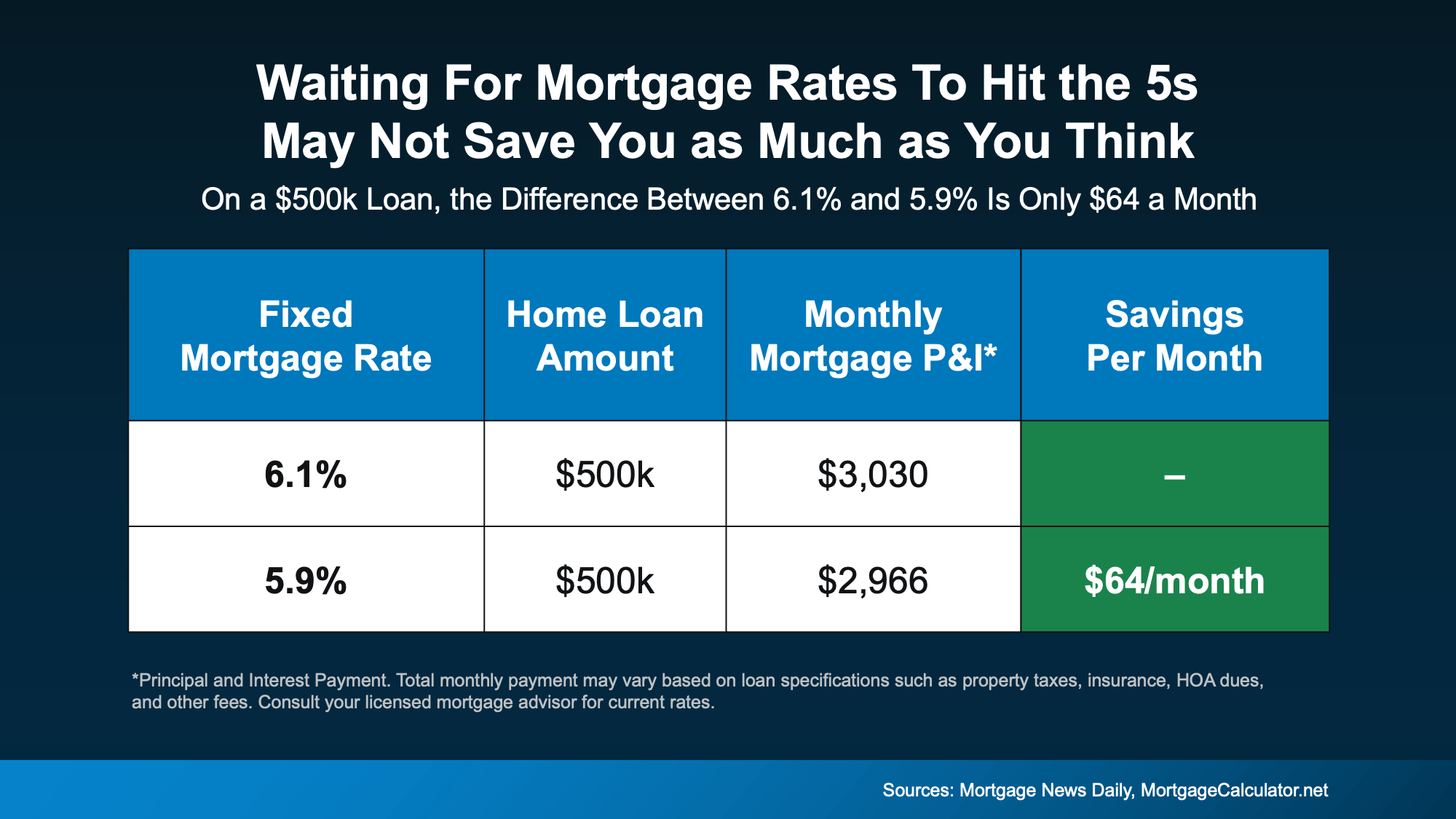

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time, that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

Yes, over time, that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

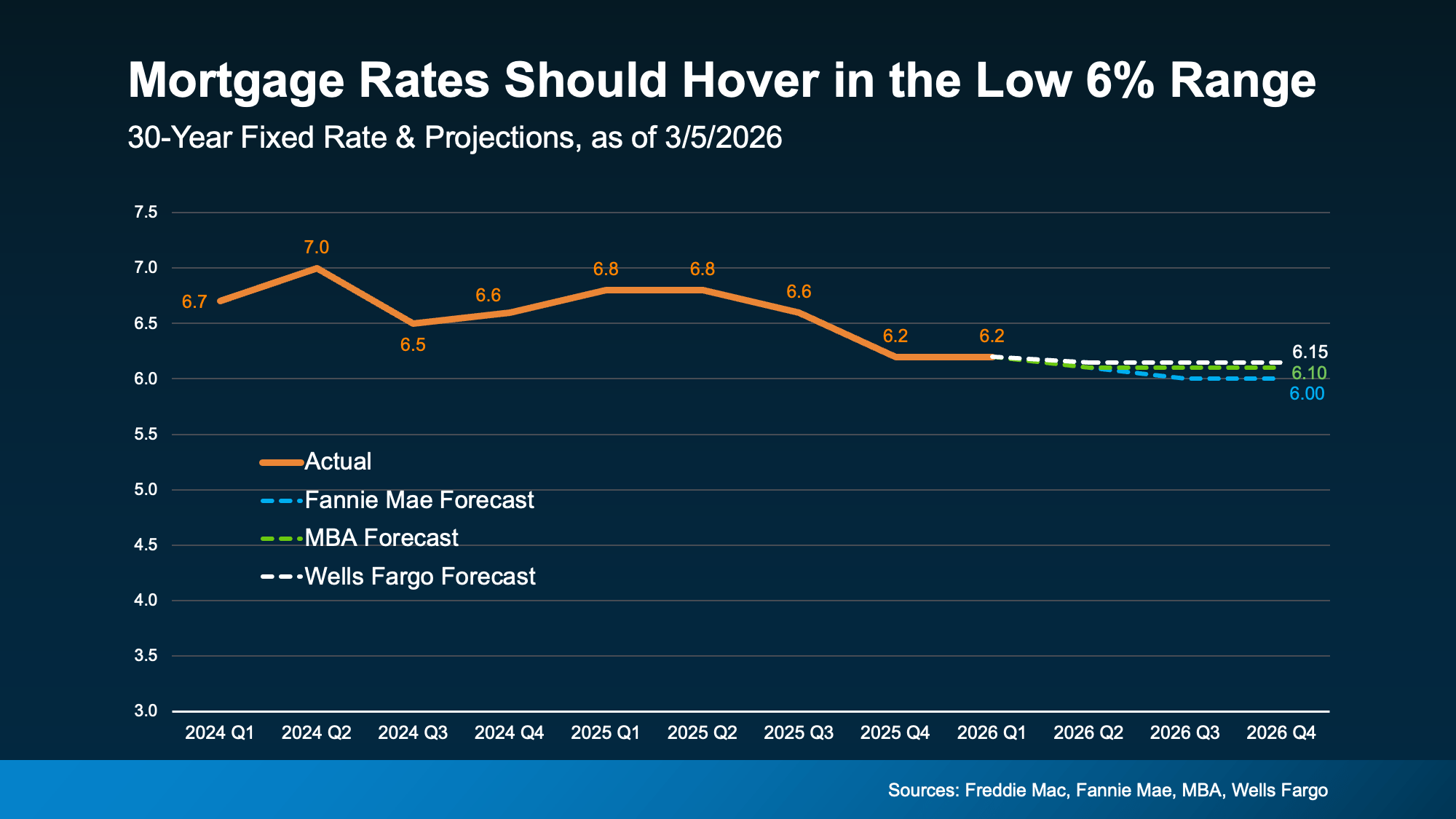

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is that waiting for a deep drop may not deliver the payoff you’re hoping for if you’re holding out

While it certainly could happen, the reality is that waiting for a deep drop may not deliver the payoff you’re hoping for if you’re holding out

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers. You may find it has never disappeared.

If you’ve been sitting on the sidelines waiting for that magic number for rates, that strategy may not pay off as much as you’d expect.

Let's connect so you can double-check the math at your price point. You may realize payments are already within your range.

This blog post previously appeared on https://www.simplifyingthemarket.com/en/2026/03/09/should-you-wait-for-lower-rates?a=106260-312309902871c1f0d820820f58bf8fde. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. and the Laura Miller Edwards Realty Group do not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. and the Laura Miller Edwards Realty Group will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Stay up to date on the latest real estate trends.

Affordability

Today's home prices have a lot of buyers wondering if there’s even anything out there that’s in their budget.

Selling Tips

Fall can offer Marietta sellers a strong window before holiday schedules begin to affect buyer activity.

Forecasts

Here's what to watch in the housing market for the second half of 2026.

Community Information

Powder Springs continues to stand out for value, particularly for buyers who prioritize square footage, larger yards, outdoor recreation, and a quieter suburban settin… Read more

For Buyers

Having student loans doesn't automatically mean buying a home has to wait.

Buying Tips

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

Community Information

Explore 2026 Fourth of July fireworks, concerts, parades, and community celebrations.

For Sellers

The sellers having the most success today are the ones who understand the market has changed and are adapting to meet it where it is.

Economy

Data shows inflation is moving in the wrong direction. But before the headlines send anyone into a panic, here's what's actually going on.

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact us today.